How Investments Grow Over Time: Compounding, Contributions, and Real Market Returns

In this guide, you'll learn:

Many investors focus on picking the “right” asset, but long-term wealth is usually driven by something much simpler: time, compounding, and consistent contributions.

A portfolio growing at 7% per year can double roughly every 10 years, turning modest investments into substantial wealth over decades.

In this guide, we break down the key forces that drive long-term portfolio growth and show how compounding, contributions, and market returns interact over time.

What Is Compound Interest in Investing?

Compound interest is one of the most powerful forces behind long-term investing. Instead of earning returns only on your original investment, compound growth allows your returns to generate additional returns over time. In simple terms, your investment begins earning returns not only on the money you invested, but also on the gains accumulated in previous years. This is why long-term investors often describe compounding as “growth on top of growth.”

At first, the effect may appear small. During the early years of an investment portfolio, most of the growth usually comes from new contributions rather than from returns themselves. However, as time passes and the portfolio becomes larger, the annual gains begin to accelerate. The longer the investment horizon, the more dramatic this compounding effect becomes. Even small differences in annual return rates can lead to significantly different outcomes after several decades.

Understanding how compounding works helps investors stay patient during slow early growth and remain focused on long-term results rather than short-term market movements. If you want to see how this effect works with different assets and time horizons, explore this example: Compound Interest Calculator: See How Gold and Bitcoin Grow Over Time .

While compound interest explains the underlying engine of long-term growth, it is also helpful to understand how this process actually unfolds inside a portfolio year by year.

How Investment Portfolios Grow Over Time

Investment portfolios rarely grow in a straight, predictable line. Instead, long-term growth usually follows a pattern where progress appears slow in the early years and accelerates later as the portfolio becomes larger. This happens because investment returns are typically applied to the total portfolio value each year. As the portfolio grows, the same percentage return produces larger and larger absolute gains.

In the beginning, most of the portfolio growth often comes from new contributions rather than investment returns. For example, an investor contributing regularly to a portfolio may see gradual increases during the first decade. Over time, however, the balance becomes large enough that annual returns start contributing a much bigger portion of the total growth. This shift is what creates the familiar “snowball effect” associated with long-term investing.

Another important aspect of portfolio growth is that markets do not move upward every year. Some years produce strong gains, while others may bring flat or negative returns. Despite this volatility, long-term portfolios have historically grown because positive market years tend to outweigh the negative ones over longer periods. Staying invested and maintaining a consistent strategy often matters more than trying to perfectly time market movements.

To better understand how portfolios evolve over time, it can be helpful to look at realistic year-by-year examples of investment growth. This detailed example shows how contributions, returns, and market fluctuations affect a portfolio across multiple years: Investment Portfolio Growth Over Time (Year-by-Year Calculator) .

Once the mechanics of portfolio growth become clear, another important insight emerges: even very small differences in annual returns can dramatically change long-term outcomes.

How Regular Contributions Accelerate Portfolio Growth

While compound returns are a powerful driver of long-term wealth, regular contributions play an equally important role in building an investment portfolio. Consistently adding money to a portfolio allows investors to increase the capital that can benefit from future market growth. Even relatively small contributions made over many years can accumulate into a significant portfolio thanks to the combined effect of saving and compounding.

In the early years of investing, contributions usually make up the largest portion of portfolio growth. When the portfolio balance is still small, market returns have a limited impact. As time passes and contributions continue, the portfolio grows larger and investment returns begin to play a bigger role. Eventually, the returns generated by the portfolio can exceed the amount added each year, which is when the compounding effect becomes much more noticeable.

Regular investing also helps smooth out the impact of market fluctuations. By investing consistently over time, investors buy assets at different price levels rather than relying on a single entry point. This approach reduces the risk of investing a large amount just before a market downturn and encourages a disciplined long-term strategy focused on steady accumulation.

A simple example can illustrate how powerful consistent investing can be. Even investing a modest amount each year can grow into a substantial portfolio over several decades. For a detailed breakdown of how contributions and compounding interact over time, see this example: What Happens If You Invest $1,000 a Year for 30 Years? .

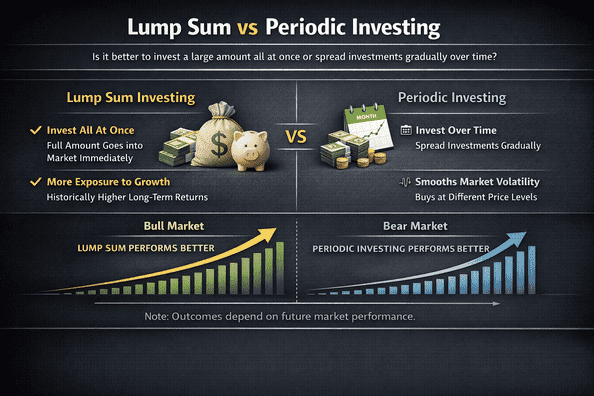

Once investors understand the value of contributing consistently, the next question becomes how those contributions should actually enter the market. Should money be invested gradually over time, or is it better to wait until a larger amount has accumulated and invest it all at once?

Lump Sum vs Periodic Investing

When beginning to invest, many people face a practical question: should they wait until they accumulate a larger amount of money and invest it all at once, or should they start investing smaller amounts regularly as soon as possible?

These two approaches are commonly described as lump sum investing and periodic investing. Lump sum investing typically means placing a large amount of money into the market at once. Periodic investing involves contributing smaller amounts on a regular schedule, such as monthly or annually.

In real life, many investors delay investing while they wait to accumulate what they believe is a meaningful amount of capital. During this waiting period, money often remains in cash, which means the portfolio is not benefiting from compounding or market growth.

Periodic investing takes a different approach. Instead of waiting, investors begin contributing smaller amounts immediately and continue investing regularly over time. This allows compounding to start earlier and helps build a consistent investing habit.

Each approach has advantages. Investing a large amount immediately can maximize the time money spends in the market, while regular contributions can reduce emotional stress and make investing easier to maintain over long periods.

To explore how contribution timing affects portfolio growth and investor behavior in more detail, see this comparison: Annual vs Lump Sum Investing: How Timing Your Contributions Impacts Portfolio Growth .

Regardless of whether investors contribute gradually or invest a larger amount later, the long-term outcome still depends primarily on the returns generated by the underlying investments.

To understand what those long-term returns typically look like, it is helpful to examine historical stock market performance.

Average Stock Market Returns (S&P 500 CAGR)

When investors think about long-term market performance, the S&P 500 is often used as a benchmark. The index tracks 500 of the largest publicly traded companies in the United States and is widely considered a representation of the overall U.S. stock market. One of the most common ways to measure its long-term performance is through the compound annual growth rate (CAGR), which shows the average yearly return over a specific period while accounting for compounding.

Historically, the S&P 500 has delivered strong long-term returns, although the exact results vary depending on the time period examined. Over several decades, the index has produced average annual returns close to about 10% before adjusting for inflation. This does not mean the market grows by the same percentage every year. In reality, stock market returns fluctuate significantly from year to year, with some years producing strong gains and others experiencing losses.

The concept of CAGR helps investors understand what a consistent annual growth rate would look like if the total return were smoothed across the entire investment period. This makes it easier to compare long-term investment performance and estimate how portfolios may grow over time. However, it is important to remember that past performance does not guarantee future results, and market returns can vary depending on economic conditions, interest rates, and global events.

To explore historical growth rates and see how the S&P 500’s compound annual growth rate has changed across different time horizons, see this detailed breakdown: S&P 500 Compound Annual Growth Rate .

While historical market returns provide a useful benchmark, even small differences in annual return rates can significantly change long-term portfolio outcomes.

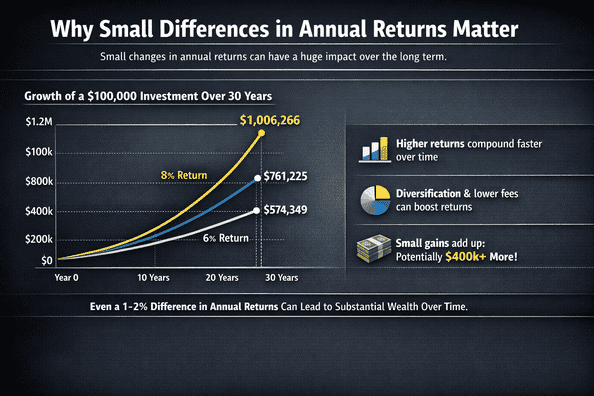

Why Small Differences in Annual Returns Matter

At first glance, a difference of just one or two percentage points in annual investment returns may not seem significant. However, over long periods of time, even small changes in the average growth rate can lead to dramatically different portfolio outcomes.

For example, a portfolio growing at 6% annually will steadily increase over time, but a portfolio growing at 7% or 8% compounds much faster. The difference may appear small in the early years, yet over multiple decades the gap between these growth rates can become surprisingly large. A slightly higher return means every future gain is calculated on a larger balance, which accelerates long-term growth.

This is one of the reasons investors pay attention to factors such as portfolio diversification, asset allocation, and investment costs. Lower fees, better diversification, or slightly higher average market returns can improve the long-term growth rate of a portfolio. Even a seemingly minor improvement in annual performance can add thousands or even hundreds of thousands of dollars to a long-term investment portfolio.

If you want to see how much impact a small change in annual returns can have over time, you can explore a detailed example here: How a 1% Change in Annual Growth Rate Can Transform Your Portfolio . This example illustrates how different growth rates affect the final value of a portfolio across multiple decades of investing.

However, nominal investment returns do not tell the whole story. To understand how much wealth actually grows over time, investors must also consider the impact of inflation.

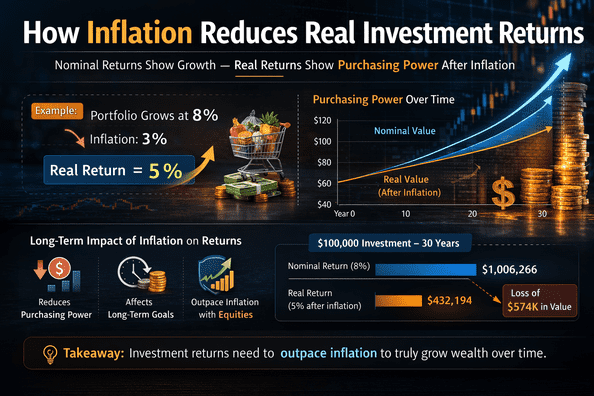

How Inflation Reduces Real Investment Returns

When evaluating investment performance, it is important to distinguish between nominal returns and real returns. Nominal returns represent the raw percentage growth of an investment, while real returns adjust that growth for inflation. Inflation gradually reduces the purchasing power of money over time, meaning that even when a portfolio grows, its true economic value may increase more slowly than it first appears.

For example, if an investment portfolio grows at 8% annually but inflation averages 3% during the same period, the real return is closer to 5%. This difference may seem modest in a single year, but over long investment horizons the impact becomes substantial. Because both inflation and investment returns compound over time, higher inflation can significantly reduce the real value of capital accumulation.

Inflation also affects how investors plan their long-term goals. A retirement portfolio that appears large in nominal terms may support less purchasing power if inflation remains elevated over several decades. This is why many long-term investment strategies emphasize assets that historically have had the potential to outpace inflation, such as diversified equity portfolios.

Understanding the relationship between inflation and investment returns helps investors set more realistic expectations for portfolio expansion. Instead of focusing only on headline returns, it is useful to consider how much purchasing power those returns actually create. To see how different inflation rates can influence long-term portfolio outcomes, explore this example: How Inflation Impacts Long-Term Portfolio Growth .

How Time Horizon Affects Investment Growth

Time horizon plays a critical role in how investment portfolios grow and how much risk investors can take. When the investment horizon is long, investors can typically focus on growth-oriented assets because short-term market fluctuations have time to recover. However, as the time horizon becomes shorter, protecting existing capital often becomes more important than maximizing growth.

During the final years before retirement, portfolios are often adjusted to reduce overall risk exposure. This may involve gradually lowering the percentage of assets allocated to equities and increasing exposure to more stable assets such as bonds, cash equivalents, or other lower-volatility investments. The goal is not to eliminate growth entirely, but to balance the need for continued returns with the need for greater stability.

Another key consideration is sequence-of-returns risk. If a major market downturn occurs shortly before or immediately after retirement begins, withdrawals from the portfolio can significantly reduce the remaining capital. Because of this risk, investors approaching retirement often prioritize diversification and portfolio resilience rather than aggressive growth strategies.

Planning a portfolio with a five-year horizon typically involves evaluating expected returns, potential market volatility, and the investor’s upcoming income needs. A more conservative allocation may help reduce the impact of short-term market swings while still allowing some participation in market growth. For a practical example of how a portfolio might be structured in the final years before retirement, see: 5 Years to Retirement Portfolio .

Frequently Asked Questions

What is compound interest in investing?

Compound interest means that investment returns generate additional returns over time. Instead of earning returns only on the initial investment, investors earn returns on both their original capital and the gains accumulated in previous years. Over long periods, this compounding effect can significantly accelerate portfolio growth.

How much do investments grow per year on average?

Historically, the S&P 500 has delivered average annual returns of about 10% before adjusting for inflation. However, returns vary from year to year, and future market performance may differ from historical averages.

Why do investment portfolios grow slowly at first?

During the early years of investing, most portfolio growth comes from contributions rather than investment returns. As the portfolio becomes larger over time, the annual returns generated by the portfolio begin to play a much bigger role in total growth.

How does inflation affect investment returns?

Inflation reduces the purchasing power of money over time. Even if a portfolio grows in nominal terms, the real value of that growth depends on how much inflation occurs during the investment period. Investors often aim to invest in assets that historically have the potential to outpace inflation.

Related:

- Compound Interest Calculator: See How Gold and Bitcoin Grow Over Time

- How to Spread Your Investments Across Stocks, Gold, Crypto & Bonds (Simple Guide)

- Why Not Just Invest in the S&P 500?

- $1,000 a Year for 30 Years: Here’s How Much You’ll Actually Have

- How Many Assets Should a Portfolio Have? Practical Guide for Investors

- Investment Portfolio Growth Over Time (Year-by-Year Calculator)

- How a 1% Change in Annual Growth Rate Can Transform Your Investment Portfolio | Portfolio Calculator

- How Inflation Impacts Long-Term Portfolio Growth

- 50% Stock Market Loss: How Long Does Recovery Take?

- How to Build a Diversified Investment Portfolio (Long-Term Strategy Guide)