Annual vs Lump Sum Investing: How Timing Your Contributions Impacts Portfolio Growth

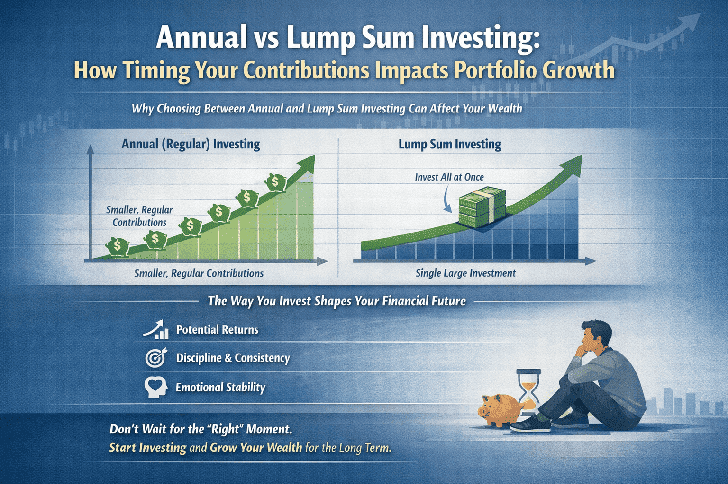

Why Choosing Between Annual and Lump Sum Investing Can Affect Your Wealth

One of the first decisions new investors face is not which asset to buy, but how to start investing. Should you wait until you have accumulated a meaningful amount of money and invest it all at once, or should you start immediately with smaller, regular contributions?

At first glance, this may appear to be a technical or secondary decision. In reality, the choice between annual (or regular) investing and lump sum investing is one of the most important factors shaping long-term portfolio growth. This decision affects not only potential returns, but also discipline, emotional stability, and the likelihood that investing actually happens at all.

Many people never start investing because they are waiting for the “right” amount of money or the “right” moment. Understanding how contribution timing affects portfolio growth can help remove this barrier and make investing more accessible.

Annual Investing vs Lump Sum Investing: Key Differences for Long-Term Returns

Opportunity Cost of Waiting to Invest

Waiting to invest a “perfect” lump sum often costs more than investing smaller amounts immediately. A common situation is that investors delay investing while they save money in cash. During this waiting period, time passes, inflation reduces the purchasing power of money, and the benefits of compounding are delayed. Even if markets remain flat, the opportunity cost of not being invested can be significant.

Benefits of Regular Contributions

With regular investing, money enters the market immediately. Smaller amounts are invested at consistent intervals, such as monthly or annually. This approach is easier to maintain over long periods and reduces the pressure of making a single, high-stakes decision.

Most importantly, compounding starts earlier. Starting early, even with smaller amounts, allows returns to build on top of previous returns over time. This compounding effect can have a dramatic impact on long-term portfolio value.

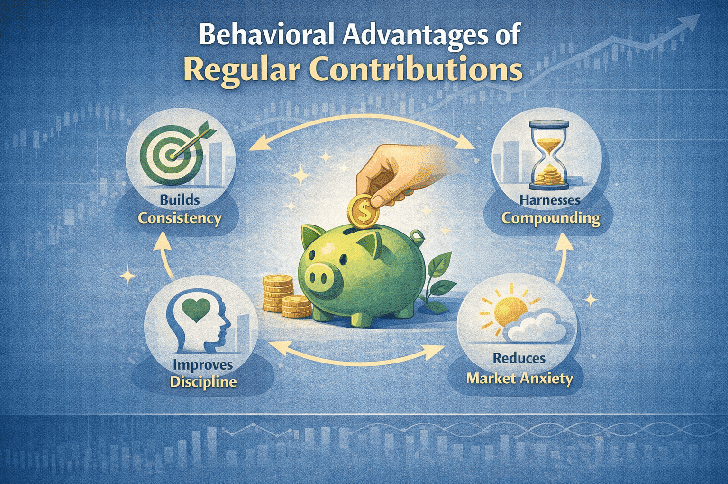

Behavioral Advantages of Regular Contributions

Why Habitual Investing Improves Discipline and Reduces Emotional Stress

When comparing regular investing vs lump sum investing, the psychological component is often underestimated. Regular contributions help build a habit. Instead of relying on motivation or perfect timing, investing becomes part of a routine. This lowers the emotional barrier and reduces the temptation to delay decisions.

Personal Experience With Procrastination

From personal experience, it is easy to postpone investing. I have often told myself that I would invest next year or after saving a bit more. Over time, excuses appear, priorities change, and the opportunity to invest early is lost. This may not apply to everyone, but for many beginners and passive investors, discipline and consistency matter more than market timing.

Emotional Challenges of Lump Sum Investing

By contrast, lump sum investing requires a high level of emotional discipline. Investing a large amount of money at once can be stressful, especially during volatile market conditions. This stress can lead to poor decisions, such as delaying investment or selling at the wrong time.

Understanding Timing Risk in Lump Sum Investing

Lump sum investing introduces significant timing risk. Timing risk refers to the possibility of investing a large amount of money just before a market downturn. If markets fall shortly after investing, the psychological impact can be severe, and recovery may take years.

While investing at the perfect moment can significantly improve returns, consistently identifying those moments requires skill, experience, emotional control, and time. For most passive investors, this combination is unrealistic.

Depending on future discipline is risky. Life circumstances change, priorities shift, and plans often do not work out as expected. Building a system that invests automatically reduces the risk of inaction and missed opportunities.

Investment Examples: Annual Investing vs Lump Sum

Example 1 – Annual Investing Over 10 Years

We start with an initial amount of $0 and invest $2,000 at the beginning of each year for 10 years. The average annual return is assumed to be 8%, which is a realistic long-term average for diversified ETF portfolios.

- Total invested: $20,000

- Investment period: 10 years

- Average annual return: 8%

- Portfolio value after 10 years: $31,290.97 (net profit $11,290.97) - You can see this in the calculator example here.

Example 2 – Waiting to Invest a Lump Sum

- Total saved: $20,000

- Investment return during waiting period: 0%

- Portfolio value after 10 years: $20,000

Comparison Table: Annual vs Lump Sum Investing

| Strategy | Total Invested | Final Value | Opportunity Cost |

|---|---|---|---|

| Annual investing | $20,000 | $31,290.97 | — |

| Waiting for lump sum | $20,000 | $20,000 | −$11,290.97 |

When Lump Sum Investing Can Be Advantageous

Scenarios Where Investing a Large Sum Immediately May Outperform Regular Contributions

If a large amount of money is invested immediately after a major market downturn, returns can be similar or even better than those achieved through regular investing.

Historical Market Examples

- 1929–1934

- 2000–2005

- 2008–2013

However, identifying these moments in real time is extremely difficult. Most investors recognize major crashes only in hindsight. Relying on such rare opportunities introduces additional risk and uncertainty.

Time in the Market vs Timing the Market

This comparison highlights one of the most important principles in investing: time in the market is often more important than timing the market. Regular investing allows money to enter the market across different conditions. Some contributions are made at higher prices, others at lower prices, but over time this smooths out volatility.

Rather than attempting to maximize returns in every possible scenario, regular investing minimizes the risk of severe mistakes that can permanently damage long-term results.

Inflation and Waiting to Invest

Money held in cash is not risk-free. Inflation gradually erodes purchasing power, meaning that the same amount of money buys less in the future. While waiting to invest, investors lose both potential investment returns and real value. Even in periods of low inflation, delaying investment can significantly reduce long-term wealth.

Situations Where Lump Sum Investing Makes Sense

- Receiving an inheritance

- Selling property or a business

- Having a very long investment horizon and high tolerance for volatility

Even in these cases, many investors choose to invest the lump sum gradually over several months to reduce timing risk and emotional stress.

Final Thoughts: Why Regular Investing Works for Most People

The greatest advantage of regular investing is not mathematical, but behavioral. Smaller, consistent contributions help build discipline, reduce emotional stress, and increase the likelihood of long-term success. For beginners and passive investors, starting early and investing regularly is often the most realistic and sustainable way to grow a portfolio over time.

Frequently Asked Questions (FAQ)

Is annual investing better than lump sum investing?

For most beginners and passive investors, regular investing reduces timing risk and improves consistency.

Does lump sum investing outperform dollar cost averaging?

Lump sum investing can outperform in rising markets, but it involves higher short-term risk and emotional pressure.

Why is time in the market important?

Because compounding requires time. The earlier money is invested, the more time it has to grow.