How a 1% Change in Annual Growth Rate Impacts Your Investment Portfolio

I'm sure that a large number of people who see the title of this article don't think they're going to read anything particularly useful. I believe that a lot of people don't know or do mathematics on a deeper level. Sometimes a small difference in numbers can make a big difference over time, which is why I wanted to write this article and explain the difference.

When investors plan for the future, they often focus on contributions and time horizon while overlooking one critical assumption: the annual growth rate. This installment is actually a percentage of the basic amount by which it is increased. Even a small change in this number can dramatically alter long-term outcomes.

This article explains why growth rates matter, how compounding amplifies small differences, and how you can test multiple scenarios using a portfolio calculator. By understanding how sensitive long-term results are to growth assumptions, you can make smarter decisions and set more realistic expectations.

How to Test Different Growth Rates Using a Portfolio Calculator

Because no one can predict future returns, testing multiple growth scenarios is smarter than relying on a single estimate. A portfolio calculator allows you to quickly compare conservative, expected, and optimistic growth rates.

Compare 7% vs 8% vs 9% portfolio growth over 30 years with starting amount 20,000.

By adjusting only the annual growth rate, you can see how sensitive your final portfolio value is to small changes. This helps you understand best- and worst-case outcomes, set contribution targets, and plan with greater confidence.

Why Even a 1% Difference Matters for Long-Term Investing

If we were to look at just one year, then a 1% difference becomes almost insignificant. In the market, swings are much larger than that. However, when we look at investing, something that is very important is a long-term plan and a long series of years over which we plan to invest our money. At least that's how it should be. In that long series of years, imagine the base for the next year that is 1% higher. Over the years, this number becomes significantly larger.

Because of compounding, a slightly higher growth rate accelerates results over time. What starts as a small gap gradually widens into a significant difference. Investors who ignore this effect often underestimate how much their portfolio could grow—or how much they actually need to save.

The Power of Compounding: How Small Growth Changes Multiply Over Time

The longer you invest, the more powerful a 1% difference becomes. Over short periods, the impact is limited. Over long periods, it can define the success of your entire strategy. Long-term investors benefit most from compounding, but they are also most exposed to incorrect growth assumptions.

A portfolio growing at 7% instead of 6% doesn’t just earn more—it earns more on an increasingly larger balance. Over 25 or 30 years, this difference can amount to tens or even hundreds of thousands as you will see in next sections.

I know it sounds incredible that a difference of only 1% can make a significant difference. Of course, if we look at it in the short term, this figure is almost insignificant. So it is insignificant if we are talking about a period of just a few years, I would even say that it is barely visible in the first 10 years of investment.

Whenever I mention investing, I mean it's a long-term plan that you want to stick to until your retirement or at least for 20 years. In periods like these, 1% can mean a lot, compounding can come into play.

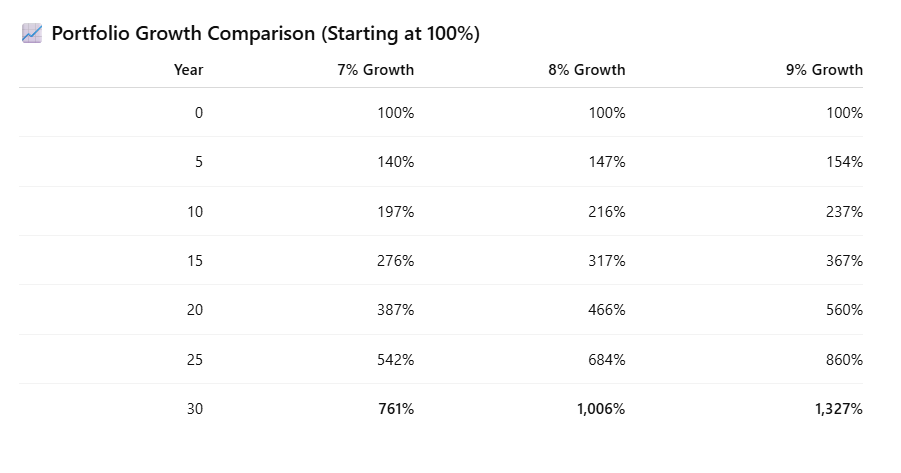

Real Portfolio Examples: Comparing 7%, 8%, and 9% Annual Growth

Consider an investor who contributes the same amount each month for 30 years. At 7% annual growth, the portfolio grows steadily but modestly. At 8%, the final value increases noticeably. At 9%, the difference becomes dramatic.

This table clearly shows the impact of just a 1% difference in annual growth over time. After 30 years of investing:

- 7% growth → portfolio grows to approximately 7.6 times the initial amount.

- 8% growth → portfolio reaches around 10 times the starting value.

- 9% growth → portfolio climbs to about 13.2 times, nearly double the result of 7% growth.

If we convert these figures into money with an initial capital of 20,000 we get the following figures:

- 7% growth → $152,245.10

- 8% growth → $201,253.14

- 9% growth → $265,353.57

Here you can clearly see how much difference 1% makes over 30 years. If the annual growth is only 1% higher, the amount we have at the end of the investment is as much as 30% higher, which in my opinion is not negligible at all.

What Happens Over 10, 20, and 30 Years of Investing

When you first start investing, the early years can feel slow and even discouraging. During the first 10 years, most of your portfolio growth usually comes from your own contributions rather than from investment returns. Because of this, a 1% difference in annual growth rate often seems insignificant, and many investors assume that small variations in returns do not really matter.

After around 20 years, the situation begins to change. Compounding becomes much more visible, and returns start to play a larger role in portfolio growth. At this point, portfolios with slightly higher growth rates begin to pull ahead in a noticeable way. What once looked like a small assumption starts to feel more meaningful, especially when comparing long-term results.

By the 30-year mark, compounding typically dominates the outcome. In many cases, the total investment returns exceed the total amount contributed over the years. A portfolio growing just 1% faster can end up significantly larger. This clearly shows how time transforms small, almost invisible differences into powerful forces that shape long-term investment success.

The Math Behind Compounding: How Small Gains Become Big Numbers

Compounding is the process by which your investment earnings begin to generate earnings of their own. In simple terms, you don’t just earn returns on your original investment—you earn returns on every previous gain as well. This creates a snowball effect that grows stronger with each passing year. Early on, compounding feels slow and almost unnoticeable. The numbers increase gradually, which often leads investors to underestimate its true power.

The key reason compounding is so powerful is that it is exponential rather than linear. A linear increase adds the same amount every year, while exponential growth increases by a percentage of an ever-growing base. When your portfolio grows by 7% one year, the next year’s 7% is calculated on a larger balance. Add just 1% more to that growth rate, and the base becomes larger every single year going forward.

Over decades, this difference compounds on top of itself. A portfolio growing at 8% doesn’t just outperform one growing at 7% by a small margin—it accelerates away from it. This is why small, seemingly insignificant gains can turn into very large numbers over long time horizons, fundamentally changing the outcome of your investment strategy.

Why Early Contributions Amplify Long-Term Growth

Money invested early has more time to compound, making early contributions especially powerful. A higher growth rate applied early multiplies results over decades.

I hate to say this, but I regret not starting investments earlier. I didn't think this way before, and I'm sure that many people my age also have the same opinion.

Even small investments made early can outperform much larger investments made later. This is why starting early is one of the most effective investing decisions you can make.

I still think to this day that I could have started investing much earlier, for example 10 years earlier when I had a much lower salary. If I had set aside a smaller amount each month, it would have been a great success and it was possible even in addition to other living expenses because I also believe that a small amount over time can bring a lot.

I do not want to advise anyone to invest, I am just telling you about my experience and I am sure that most of us who have an regular and normal job can afford it.

Conclusion: Small Assumptions, Big Long-Term Impact

At first glance, a 1% difference in annual growth doesn’t seem worth much attention. In a single year, it is barely noticeable and easily lost in normal market fluctuations. But as this article shows, investing is not about one year — it is about decades.

The goal is not to chase unrealistic returns, but to understand how sensitive long-term outcomes are to reasonable assumptions. Lower fees, disciplined investing, diversification, and time in the market often matter more than trying to predict short-term performance.

By understanding how a 1% change affects your portfolio, you gain clarity. And clarity — not prediction — is what allows for better planning, realistic expectations, and more confident long-term decisions.