How to Build a Diversified Long-Term Investment Portfolio (Allocation & Rebalancing Guide)

Quick Summary:

- A diversified portfolio typically includes 3–7 assets across different classes.

- Stocks drive long-term growth, while bonds, gold, and cash provide stability.

- Rebalancing helps maintain your target allocation and control risk.

- Long-term investing relies on compounding and consistent contributions.

Table of Contents

- What Is a Long-Term Investment Portfolio?

- Why Diversification Is the Foundation of Portfolio Stability

- How Many Assets Should a Portfolio Have?

- Aggressive vs Conservative Allocation Strategies

- Should You Just Invest in the S&P 500?

- S&P 500 vs Nasdaq 100 – Understanding the Difference

- The Importance of Portfolio Rebalancing

- How Inflation Impacts Long-Term Portfolio Growth

- How Contributions and Time Horizon Shape Portfolio Results

- How to Design Your Own Portfolio Strategy

- Frequently Asked Questions

What Is a Long-Term Investment Portfolio?

A long-term investment portfolio is a structured collection of assets designed to grow wealth over an extended period — typically 10, 20, or even 30+ years. Instead of relying on a single stock or asset, a portfolio combines multiple investments such as broad market index funds, sector ETFs, bonds, or alternative assets. The goal is not short-term speculation, but steady capital growth through compounding over time.

The primary purpose of a long-term portfolio is wealth building. It can support major life goals such as retirement, financial independence, funding education, or creating generational wealth. Because the time horizon is long, investors can tolerate short-term market volatility in exchange for higher expected long-term returns. Time becomes a strategic advantage: downturns are temporary, but compounding is permanent.

At the core of every portfolio lies the risk-versus-return framework. Higher expected returns usually come with higher volatility and deeper drawdowns. Lower-risk assets may provide stability but typically generate slower growth. A well-designed portfolio balances these trade-offs based on an investor’s time horizon, financial goals, and psychological comfort with market fluctuations.

Structure matters because random investing often leads to inconsistent results. Without a clear allocation strategy, portfolios can become unintentionally concentrated in one sector, geography, or asset class. Over time, this concentration increases risk. A structured portfolio, on the other hand, defines target allocations, manages exposure deliberately, and creates a repeatable investment process. That structure is what transforms investing from guessing into disciplined wealth building.

Why Diversification Is the Foundation of Portfolio Stability

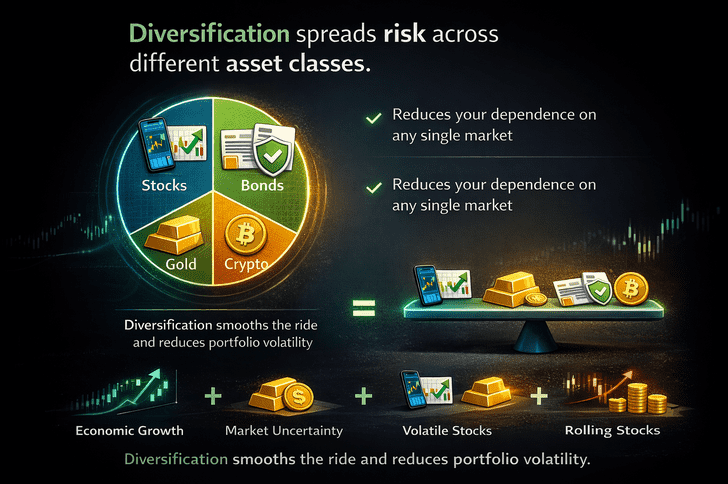

Diversification is one of the most important principles in long-term investing because it reduces the impact of any single asset on your overall portfolio. Instead of concentrating all your capital in one investment — whether that’s gold, an ETF, or cryptocurrency — diversification spreads risk across multiple asset classes. If you want a detailed, step-by-step explanation of how to structure this properly, see How to Create a Diversified Portfolio.

A diversified portfolio typically includes different asset classes such as stocks, cryptocurrencies, precious metals like gold, and bonds or cash equivalents. Each asset class behaves differently under various market conditions. Stocks may perform strongly during economic expansion, gold often acts as a hedge during uncertainty, and bonds can provide stability when equity markets are volatile. By combining them, you avoid depending entirely on the performance of a single market.

The key concept behind diversification is correlation. Correlation measures how assets move relative to one another. If two assets are highly correlated, they tend to rise and fall together. True diversification comes from combining assets with low or moderate correlation, so that when one declines, another may remain stable or even increase. This reduces the overall volatility of your portfolio.

Lower volatility doesn’t necessarily mean lower returns. Instead, diversification aims to smooth returns over time, making it easier to stay invested during market downturns. A stable structure helps investors avoid emotional decisions, maintain discipline, and stay focused on long-term growth rather than short-term fluctuations.

How Many Assets Should a Portfolio Have?

There is no perfect number of assets that guarantees success, but there is a practical range that works for most long-term investors. If you want a deeper breakdown with real-world examples, you can read the full guide here: How Many Assets Should a Portfolio Have?.

The key idea is balance — not maximum quantity.

For most individual investors, a 3–7 asset model provides an effective mix of diversification and simplicity. With three to seven carefully selected assets, you can cover different economic scenarios without creating unnecessary complexity. For example, a portfolio might include a broad stock ETF, bonds or cash, gold, real estate exposure, and a small allocation to cryptocurrency. Each asset plays a specific role: growth, stability, inflation hedge, or diversification. This structure reduces dependency on a single outcome while remaining manageable.

Problems begin at both extremes. Too few assets create concentration risk. If you hold only one or two investments, your portfolio becomes highly sensitive to specific market events. On the other hand, over-diversification can dilute performance and reduce clarity. Holding 15–20 similar assets often adds overlapping exposure, increases transaction costs, and makes rebalancing more difficult. More assets do not automatically mean better diversification — especially if they behave similarly during crises.

Another important consideration is ETFs versus individual stocks. Broad ETFs already contain dozens or hundreds of companies, providing built-in diversification with a single position. Individual stocks require more monitoring and increase company-specific risk. For most long-term investors, combining a few diversified ETFs with selected alternative assets offers a cleaner, more efficient structure than holding many separate securities.

Aggressive vs Conservative Allocation Strategies

Choosing between an aggressive and conservative allocation is not just about numbers — it’s about sustainability. If you want a detailed comparison with examples and expected returns, see the full breakdown here: Aggressive vs Conservative Portfolios: Risk, Returns, and Examples.

The right allocation is the one you can maintain during both strong bull markets and painful downturns.

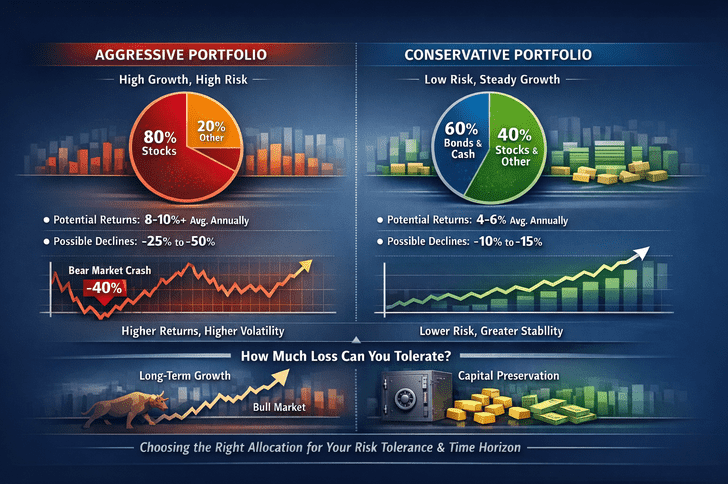

The starting point is risk tolerance. Aggressive portfolios typically hold a higher percentage of equities or high-growth assets, which can generate stronger long-term returns but also experience significant volatility. A 25–50% temporary decline is possible in aggressive allocations. Conservative portfolios, on the other hand, include more bonds, cash equivalents, or broadly diversified ETFs, reducing volatility but also lowering expected returns. The key question is not “How much can I earn?” but “How much loss can I tolerate without panic selling?”

Many investors also use age-based models as a practical guideline. Younger investors with a long time horizon can often afford more aggressive allocations because they have decades to recover from market declines. Investors approaching retirement typically shift toward more conservative allocations to protect capital and reduce sequence-of-returns risk. Time horizon often matters more than personality alone.

Historical data reinforces this trade-off. Aggressive portfolios have delivered higher long-term average returns, but they also experienced deeper historical drawdowns, such as the 2008 financial crisis or sector-specific collapses. Conservative portfolios fell less during these periods but grew more slowly over time. Ultimately, the best allocation is not the one with the highest theoretical return — it’s the one you can stick with consistently through market cycles.

Should You Just Invest in the S&P 500?

The idea of investing only in the S&P 500 is attractive for a reason. It offers strong historical returns, exposure to large and profitable U.S. companies, low costs, and minimal effort. For many investors, especially beginners and those prioritizing simplicity, this simplicity argument can feel very compelling. If you want a deeper breakdown of both the advantages and hidden risks, check out this full article: Why Not Just Invest in the S&P 500?.

However, simplicity does not eliminate risk. One of the main concerns with relying solely on the S&P 500 is concentration risk. While the index technically contains 500 companies, it is weighted by market capitalization — meaning the largest companies carry the most influence. In recent years, the top 10 stocks have accounted for roughly one-third of the index’s total weight. If those biggest names decline significantly, the entire index can suffer even if smaller components are relatively stable. This makes the index less diversified in practice than it appears on the surface.

Another important factor is US-only exposure. Although many S&P 500 companies generate significant global revenue, the index itself is tied to the U.S. economy, regulation, and currency. For investors outside the United States, fluctuations in the U.S. dollar can meaningfully affect your real returns. A strong dollar might reduce gains when converted back to your local currency, while a weak dollar might improve them — but either outcome adds another layer of uncertainty.

Investing solely in the S&P 500 can be appropriate in some scenarios — especially if you have a long time horizon and are comfortable with short-term volatility. But for many investors, diversifying beyond a single index can reduce concentration and regional risks while still capturing long-term growth potential.

S&P 500 vs Nasdaq 100 – Understanding the Difference

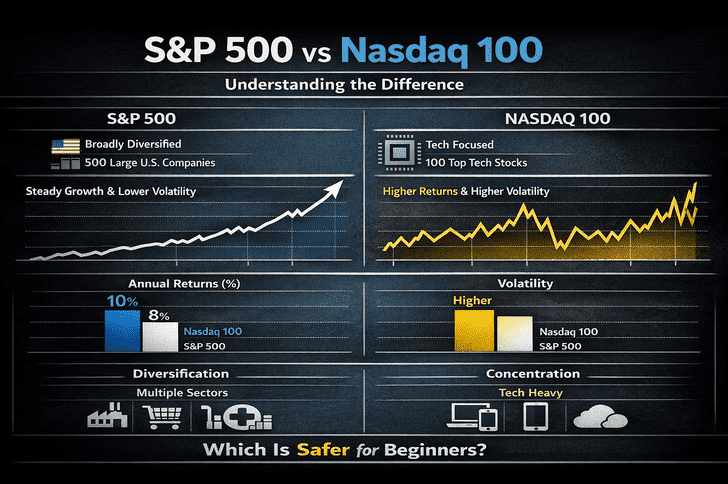

For many beginner investors, one of the first important decisions is choosing which broad market index to invest in. Two of the most widely discussed options are the S&P 500 and the Nasdaq 100. While both track large and influential companies in the U.S. stock market, they differ significantly in diversification, sector exposure, and volatility. If you want a deeper look at which of these indexes may be safer for beginners, you can explore this detailed comparison: S&P 500 vs Nasdaq 100: Which Is Safer for Beginners?.

Performance and Volatility Differences

Historically, the Nasdaq 100 has achieved higher average annual returns than the S&P 500. Much of this growth has been driven by the expansion of major technology companies over the past few decades.

However, higher potential returns usually come with greater volatility. Because the Nasdaq 100 is more concentrated in fewer sectors, its price movements tend to be larger during both market rises and market downturns.

Diversification vs Concentration

The key difference between these two indexes comes down to diversification versus concentration. The S&P 500 spreads risk across many sectors of the economy, while the Nasdaq 100 focuses more heavily on technology-driven growth.

Understanding these differences helps investors choose the index that best fits their investment goals, time horizon, and tolerance for market volatility.

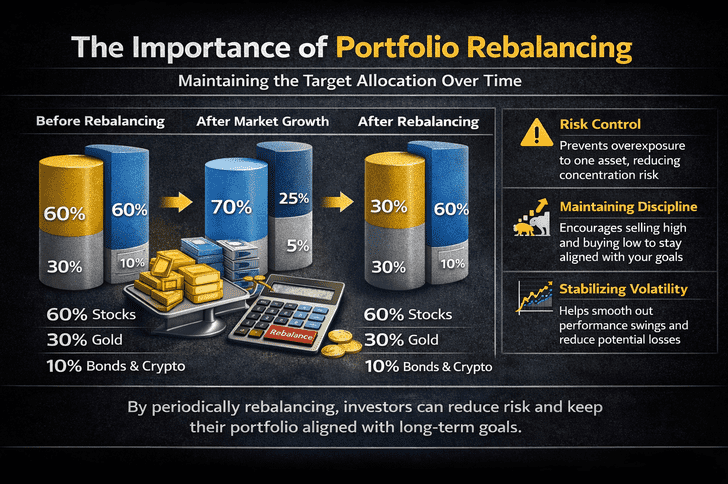

The Importance of Portfolio Rebalancing

Portfolio rebalancing is a key concept in long-term investing. When investors build a portfolio, they usually start with a target allocation between different assets such as stocks, gold, bonds, or cryptocurrencies. Over time, markets move differently and those allocations begin to change. Some assets grow faster than others, while others may stagnate or decline. As a result, the original balance of the portfolio gradually drifts away from the intended structure.

Rebalancing is the process of restoring the portfolio back to its target allocation. For example, an investor might initially decide to allocate 60% to stocks, 30% to gold, and 10% to other assets. After a strong market year, stocks could grow to represent 70% of the portfolio while other assets shrink in proportion. Rebalancing would involve reducing the overweight asset and increasing the underweight ones to return the portfolio to its planned allocation.

The main purpose of portfolio rebalancing is risk control. When one asset grows significantly, the portfolio can become overly dependent on that single investment. This increases concentration risk and exposes the investor to larger potential losses if that asset later declines. By periodically rebalancing, investors keep their risk profile aligned with their original investment plan.

Another benefit of rebalancing is maintaining discipline. Investors often feel tempted to keep buying assets that have recently performed well while ignoring those that have lagged. Rebalancing encourages a more structured approach by trimming assets that have grown too large and reallocating funds toward those that now represent a smaller portion of the portfolio.

Rebalancing does not guarantee higher returns. In strong bull markets it can even slightly reduce gains because it requires selling part of the best-performing assets. However, its true value lies in stabilizing volatility and keeping the portfolio aligned with long-term goals.

If you want to explore this topic in more detail, including practical examples and strategies for when to rebalance, you can read a full guide on portfolio rebalancing here: Portfolio Rebalancing: How Often Should You Rebalance?.

How Inflation Impacts Long-Term Portfolio Growth

When planning long-term investments, most people focus on how much money their portfolio might grow in the future. However, one of the most important factors investors often overlook is inflation. Inflation gradually reduces the purchasing power of money, meaning the same amount of money buys fewer goods and services over time. Understanding this effect is essential when estimating the real value of future investments.

Many investors calculate potential returns and feel satisfied when they see large numbers projected years into the future. But without accounting for inflation, these projections can be misleading. What matters is not just how much money you accumulate, but what that money will actually be able to buy when you eventually use it.

A simple example illustrates this idea. Imagine you had $100 ten years ago. If inflation averaged around 3% annually, the purchasing power of that same $100 would drop significantly over time. Even though the number printed on the bill stays the same, the real value declines, meaning you can buy fewer goods with it than before.

Inflation becomes even more important when planning long-term financial goals such as buying a home or building retirement savings. For instance, if a house costs $300,000 today, the price may be much higher in five or ten years due to inflation. This means simply saving money may not be enough to reach the same financial target later.

Because of this, investors often rely on assets that historically grow faster than inflation, such as stocks or diversified portfolios. These investments aim not only to preserve the nominal value of money but also to maintain or increase its real purchasing power over time.

If you want to explore this topic in more detail and see practical examples of how inflation changes long-term investment outcomes, you can read a full explanation here: How Inflation Impacts Long-Term Portfolio Growth.

Understanding inflation is a crucial step toward realistic financial planning. When evaluating portfolio growth, always consider both the nominal return and the real value of money after inflation.

How Contributions and Time Horizon Shape Portfolio Results

What Happens If You Invest $1,000 a Year for 30 Years?

Investing $1,000 per year may not sound like a large strategy, but over long periods it can grow into a meaningful portfolio thanks to compound growth. When you invest regularly, your money doesn’t just grow from new contributions—it also grows from the returns generated on previous gains. Over time, this compounding effect becomes the main driver of portfolio growth.

If you invest $1,000 every year for 30 years, your total contribution would be $30,000. However, the final value of the portfolio can be much higher depending on the average annual return of the investments. With moderate long-term returns, the ending value can be several times larger than the amount you originally invested. This difference happens because each year’s earnings remain invested and continue generating additional returns.

Another important factor is consistency. Regular contributions steadily increase the base on which compounding works. In the early years, growth usually appears slow because most of the portfolio value comes from your own deposits. But as the investment balance grows, the accumulated gains begin contributing more and more to the total growth. Over decades, this acceleration can significantly increase the final portfolio value.

This simple scenario illustrates two core investing principles: time in the market and consistent investing. Starting earlier allows compounding to work for more years, while regular contributions help smooth market fluctuations and steadily build wealth. Even relatively small yearly investments can produce substantial results when given enough time to grow.

If you want to explore this example in more detail, see the full explanation in the article: What Happens If You Invest $1,000 a Year for 30 Years?

How to Design Your Own Portfolio Strategy

Designing a portfolio strategy is not about finding a single “perfect” allocation. Instead, it is about creating a structure that fits your risk tolerance, investment horizon, and long-term financial goals. Different investors will naturally arrive at different portfolio compositions depending on how much volatility they can tolerate and how long they plan to stay invested.

A common starting point is to divide a portfolio between assets that serve different roles. For example, stocks are typically used for long-term growth, while assets such as gold, bonds, or cash equivalents can provide stability or protection during market uncertainty. By combining multiple asset classes, investors can reduce the risk that a single market movement will significantly damage their entire portfolio.

Portfolio allocation also evolves over time. Younger investors with long time horizons often choose portfolios that emphasize growth assets such as equities. Investors who are closer to their financial goals may gradually shift toward more conservative allocations in order to reduce volatility and protect accumulated gains.

Another important part of building a strategy is understanding how different allocations may behave under various market conditions. Some combinations may produce higher long-term returns but come with larger drawdowns. Others may grow more slowly but offer smoother performance and lower risk during downturns. The goal is not to eliminate risk completely, but to choose a structure that allows you to remain invested even when markets become volatile.

Because every portfolio behaves differently depending on asset allocation, it can be helpful to test different scenarios before committing real money. Exploring possible outcomes allows investors to better understand how small changes in allocation can influence long-term portfolio growth.

If you want to experiment with different asset combinations and visualize how portfolios may grow over time, you can test your ideas using this portfolio growth calculator: Portfolio Growth Calculator

Frequently Asked Questions

What is a good diversified portfolio?

A well-diversified portfolio typically includes multiple asset classes such as stocks, bonds, gold, and other investments. Diversification helps reduce risk and smooth long-term returns.

How many assets should a portfolio contain?

Many investors use a portfolio with 3–7 assets. This range provides diversification without unnecessary complexity.

Is the S&P 500 enough for diversification?

The S&P 500 provides exposure to large US companies, but it still represents a single market. Some investors diversify further with international assets, bonds, or alternative investments.

How often should a portfolio be rebalanced?

Many investors rebalance once per year or when allocations drift significantly from the target percentage.

Related:

- Compound Interest Calculator: See How Gold and Bitcoin Grow Over Time

- How to Spread Your Investments Across Stocks, Gold, Crypto & Bonds (Simple Guide)

- Why Not Just Invest in the S&P 500?

- $1,000 a Year for 30 Years: Here’s How Much You’ll Actually Have

- How Many Assets Should a Portfolio Have? Practical Guide for Investors

- Investment Portfolio Growth Over Time (Year-by-Year Calculator)

- How a 1% Change in Annual Growth Rate Can Transform Your Investment Portfolio | Portfolio Calculator

- How Inflation Impacts Long-Term Portfolio Growth

- 50% Stock Market Loss: How Long Does Recovery Take?

- How Investments Grow Over Time: Compounding, Contributions, and Real Returns