How Many Assets Should a Portfolio Have?

Investors often ask how many assets are “enough” to build a proper portfolio. The real answer depends less on theory and more on practicality: diversification, manageability, and cost efficiency.

My personal portfolio consists of 5 assets:

- real estate

- S&P 500 ETF

- gold

- cryptocurrency

- bank account earning interest

I think it has solid diversification since the S&P 500 with cryptocurrency on one side is complementary to gold on the other side. It doesn't have to be always true, but what I noticed is when gold goes steeply up, the S&P 500 usually stagnates or goes down. In this way, the portfolio is protected from uniformity.

Real estate is typically independent from all other assets. The disadvantage is not so high liquidity as other assets.

Earning interest through a bank account is constant, though I don't think it is good for portfolio growth.

This article focuses on real-world portfolio construction — not academic models — and explains how the number of assets affects risk, control, and long-term outcomes. If you want to check how your multiple assets portfolio behave during the time, you can use portfolio calculator to estimate income.

The Practical Purpose of Multiple Assets

Holding multiple assets serves one goal: reducing dependency on a single outcome. If one asset underperforms, others can offset part of the loss.

In practice, this usually means combining assets that respond differently to economic conditions, such as stocks, bonds, gold, or cash.

Adding assets beyond that point only helps if they behave differently. Otherwise, complexity increases without meaningful benefit. What I mean by this is imagine having everything invested in the S&P 500, silver, and bitcoin. Usually in a crisis, gold goes up and industry stagnates or goes down, which means that you take a risk with S&P 500 ETF, silver, and Bitcoin. These assets typically don't perform well during this time, although you invested in 3 different assets. In my opinion, this is not good for portfolio diversification unless you are convinced and expect industry growth in the next months or years.

Too Few Assets: Concentration Risk

A portfolio with one or two assets is highly sensitive to specific events. Even strong assets can go through long periods of underperformance.

Example:

- 100% stocks → exposed to market crashes. If industry goes down, then the value of your portfolio goes down accordingly. Very famous is so called “lost decade ETF” when the S&P ETF produced no rise in the period 2000–2009—0 annual growth. So imagine having no profit in this period and that is nominally. Real value is even worse due to inflation.

- 100% real estate → illiquidity risk. Real estate requires more time to sell than other assets.

- 100% gold → long flat periods - for example, if you invested in gold in 2011, in the year 2020 you would have the same nominal price. Real value would be even lower due to inflation. As an investor, we would like to avoid this situation.

With too few assets, timing matters too much — and timing is rarely reliable.

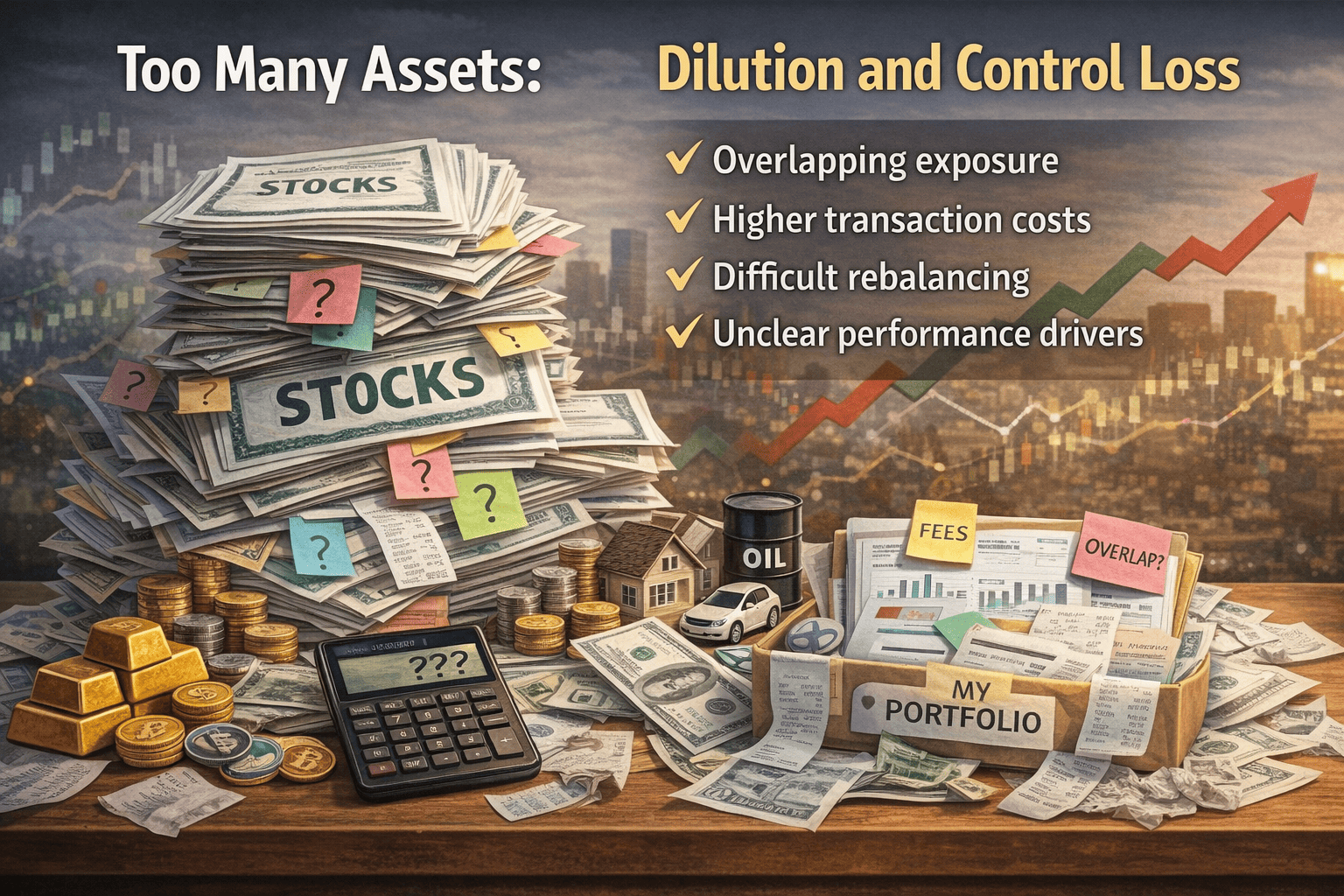

Too Many Assets: Dilution and Control Loss

On the other extreme, portfolios with 15–30 assets often suffer from:

- Overlapping exposure

- Higher transaction costs

- Difficult rebalancing

- Unclear performance drivers

If assets move similarly, adding more does not improve diversification. It only dilutes conviction and increases maintenance.

A Realistic Sweet Spot: 3 to 7 Assets

For most individual investors, a portfolio of 3 to 7 assets offers the best balance between diversification and simplicity.

This range is large enough to spread risk but small enough to:

- Understand what you own

- Track performance accurately

- Rebalance efficiently

Common examples include combinations of:

- Stocks

- Bonds

- Gold

- Cash

- Real estate exposure

- Cryptocurrency (optional, small allocation)

Example Portfolio Structures

3-Asset Portfolio

- Stocks

- Bonds

- Cash or Gold

Simple, low maintenance, and easy to rebalance.

5-Asset Portfolio

- Domestic stocks

- International stocks

- Bonds

- Gold

- Cash

Balanced exposure with clear roles for each asset.

7-Asset Portfolio

- Domestic stocks

- International stocks

- Emerging markets

- Bonds

- Gold

- Real estate

- Cash

More granular control comes with a 7-asset portfolio, but it requires discipline: Managing multiple assets means regularly monitoring each investment, rebalancing allocations, and staying focused on long-term goals. Without consistent attention and a clear strategy, it’s easy for the portfolio to drift from its intended risk and return profile.

When Adding an Asset Makes Sense

Adding a new asset to your portfolio shouldn’t be random or trendy. Every addition should have a clear purpose and benefit. A new asset makes sense only if it meets key criteria:

- Behaves differently from existing assets: Diversification is key. Assets that react differently to market changes reduce overall risk. For example, adding gold to a stock-heavy portfolio can help protect against downturns.

- Improves risk-adjusted returns: High returns alone aren’t enough. The asset should boost your portfolio’s efficiency, giving better growth for the level of risk taken.

- Has a clear role in the portfolio: Whether it’s for income, growth, or hedging, you should know exactly why this asset belongs. If you can’t explain it, it probably shouldn’t be there.

In short, every asset should earn its place. Thoughtful additions help your portfolio stay balanced, maximize long-term growth, and reduce unnecessary risks. A well-chosen asset not only diversifies your investments but also strengthens your overall strategy, keeping your financial goals on track.

Conclusion

There is no perfect number of assets, but there is a practical range. I personally have 5 assets, and I want to do adjustments during the time, but not so much in the number of assets but their percentage in the portfolio. If one asset rises too much in a short period, I like to do rebalancing.

For most investors:

- Too few assets increases risk

- Too many assets reduces clarity: A portfolio with too many investments can confuse performance tracking and risk assessment, making it harder to see which assets truly drive returns. Simplifying the portfolio helps investors maintain control, rebalance efficiently, and make smarter decisions.

- 3 to 7 assets offers balance

A well-structured portfolio is not about quantity. It’s about intentional diversification and disciplined execution.

You know what best works for you, how patient and risk-prone you are. Consistency over time and portfolio diversification can improve income during a time.