How Often Should You Rebalance a Portfolio? (5–10% Rule Explained)

Short answer: Rebalance your portfolio once per year or whenever your asset allocation drifts by more than 5–10%.

Most investors either rebalance too often (reducing returns) or not at all (increasing risk). The optimal strategy is a simple combination of time-based and threshold-based rebalancing.

What Is the 5–10% Rebalancing Rule?

The 5–10% rule means you rebalance your portfolio whenever an asset drifts more than 5–10 percentage points from its target allocation.

For example, if your target allocation for stocks is 60% and it grows to 70%, your portfolio has drifted by 10% and should be rebalanced.

This approach helps you avoid unnecessary trading while still controlling risk effectively.

Portfolio Rebalancing Example: Gold, S&P 500 and Bitcoin

I will take the example of my portfolio which contains gold, S&P 500 and bitcoin. It actually contains real estate and a fixed-term deposit account, but for simplicity of calculation I will take into account these 3 assets in these percentages:

- S&P 500 - 60%

- Gold - 33%

- Bitcoin - 7%

If you want to see how different asset allocations may affect your long-term returns, you can test various scenarios using Investment Growth Calculator and compare outcomes over 10, 20 or 30 years.

After the last year of investment (currently March 2026), gold has jumped by a huge percentage - more than 50% compared to the value of a year ago. S&P 500 stocks have risen but since I invested in euros I have come to the conclusion that the value of stocks has mostly stagnated in the last year as the dollar has weakened against the euro.

Eventually bitcoin lost quite a bit of its value. Although I have the least amount of money invested in this asset, there is still a certain loss.

So, after a year, the percentages of these assets have changed quite a bit due to the sudden growth of gold, the stagnation of the S&P 500 and the fall of Bitcoin, so that now gold occupies the entire 50% of the portfolio, which was certainly not my original plan, considering that ETFs like the S&P 500 are destined for the greatest portfolio growth and the role of gold is protected from inflation.

In the new situation I want to change the current percentages:

- Gold - 50%

- S&P 500 - 45%

- Bitcoin - 5%

Check estimated growth for changed portfolio based on historical data using Investment Growth Calculator .

How to Rebalance a Portfolio

In order to change the share of different assets in the portfolio, it is necessary to rebalance. My idea is to reduce the share in gold and increase the share in the S&P 500. This can be done in two ways:

- redirect new investments to assets that you want to occupy a larger percentage of the portfolio

- withdraw funds from the existing asset in the portfolio that you want to occupy a smaller percentage (gold) and redirect it to the asset that you want to strengthen (in my case S&P 500)

Both methods have their advantages and disadvantages, but in my opinion, a quick and easy rebalancing would be the latter to transfer investments from one asset to another in order to obtain the desired percentage. You don't need an additional investment for that, but subtract, for example, 15% from gold and add it to the S&P 500 index so that you get:

- Gold - 35%

- S&P 500 - 60%

- Bitcoin - 5%

The disadvantage of this approach is the loss of the difference in taxes from the sale of gold, since the dealers take a certain percentage during the purchase. On the other hand, it does not require you to have extra money with you or to wait to accumulate it.

The Psychology Behind Portfolio Rebalancing

What I have noticed is that the human psyche tends not to touch what currently gives results. For example, gold has risen sharply lately, so many people come to the conclusion that they should continue investing in it instead of other assets because it currently brings them a higher return, and why would they invest in assets that are currently stagnating, declining or giving a lower return. This can be a trap and does not necessarily mean that the same trend will continue in the following period.

It is difficult to predict how asset prices will move, but historically, stocks should give a higher return than gold, and the fact that gold has been giving a higher return lately does not mean that it will be so in the future. Some example when gold stagnated for ten years is the period 1980-1990 (the most famous "lost decade" of gold) and also in the period from 2011-2019 it also stagnated. In 2011 it had a value of 1900 dollars per ounce and in 2015 it fell to 1050 dollars. That's a big dropdown.

No one can say with certainty how the price of gold will move, and the fact that it is currently on a high rise does not necessarily mean that it will continue. It is certainly up to you to decide how you want to organize and rebalance your portfolio.

How Often Should You Rebalance Your Portfolio?

A good question is when and how often to rebalance. There are several approaches in this case:

Calendar-Based Portfolio Rebalancing Strategy

- once a year (most often)

- twice a year

- quarterly

The advantage of this rebalancing is that it is easy, simple and predictable.

Threshold-Based Portfolio Rebalancing Strategy

Rebalance when the drift rises above a certain X percent.

For example when 60% becomes 65 or 70%. In this way, unnecessary exchanges are avoided. The bad thing is that it requires constant monitoring.

Hybrid Portfolio Rebalancing Strategy

It represents a combination of the previous two. For example, check once a year or when the drift grows over 5%.

When Should You Not Rebalance Your Portfolio?

Although portfolio rebalancing is an important risk management tool, there are situations where rebalancing may not be optimal. In some cases, the costs or tax consequences can outweigh the benefits of restoring your target allocation.

1. High Transaction Costs

If buying and selling assets involves significant fees, spreads, or brokerage commissions, frequent rebalancing can reduce your overall returns. For example, physical gold dealers often charge buy/sell spreads, and some platforms apply trading commissions.

In such cases, small allocation drifts may not justify the cost of rebalancing. It may be more efficient to wait for a larger deviation or use new contributions to gradually restore balance instead of selling assets.

2. Taxable Investment Accounts

Rebalancing inside a taxable account can trigger capital gains taxes. Selling an asset that has appreciated significantly may result in an immediate tax liability.

Before rebalancing, consider:

- The size of the unrealized gain

- Your current tax bracket

- Whether long-term or short-term capital gains apply

In some situations, it may be more tax-efficient to rebalance using new investments rather than selling existing positions.

3. Very Small Portfolios

If your portfolio is relatively small, transaction costs and taxes can represent a meaningful percentage of total capital. In early stages of investing, maintaining a perfect allocation is less important than building consistent contribution habits.

For small portfolios, gradual rebalancing through new contributions is often sufficient. As the portfolio grows, more precise allocation management becomes more relevant.

In summary, rebalancing should always be evaluated in context. The goal is risk control — not mechanical trading. If the costs exceed the risk reduction benefit, waiting may be the smarter decision.

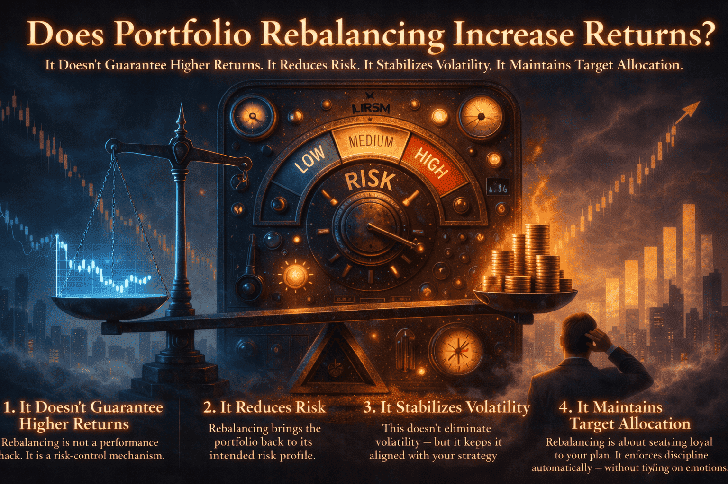

Does Rebalancing Improve Returns or Just Reduce Risk?

- it doesn't guarantee higher returns.

- it reduces risk.

- it stabilizes volatility.

- it maintains target allocation.Does Rebalancing Increase Returns?

This is one of the most common misunderstandings about portfolio management.

Many investors assume that rebalancing is a strategy designed to boost performance. In reality, its primary purpose is not to maximize returns — but to manage risk and maintain discipline.

Let's break it down.

1️. It Doesn't Guarantee Higher Returns

Rebalancing does not magically increase long-term growth. In a strong bull market, especially when one asset class (like equities) consistently outperforms others, rebalancing can actually:

- Slightly reduced returns

- Because you are trimming the best-performing asset

Example: If stocks keep rising for years, and you repeatedly sell part of them to buy bonds, your total return may end up lower than a portfolio that simply lets stocks dominate. Rebalancing is not a performance hack. It is a risk-control mechanism.

2️. It Reduces Risk

Over time, portfolios drift. A 60/40 portfolio can quietly become 75/25 after several strong equity years. That means:

- Higher volatility

- Higher downside risk

- Larger drawdowns in crashes

Rebalancing brings the portfolio back to its intended risk profile. It prevents accidental risk escalation. Without rebalancing, your portfolio slowly turns into something you never intended to own.

3️. It Stabilizes Volatility

When one asset grows much faster than others, the portfolio becomes more concentrated. Concentration increases volatility. By trimming outperforming assets and adding to underperformers, rebalancing:

- Smooths return swings

- Reduces extreme portfolio behavior

- Improves consistency

This doesn't eliminate volatility — but it keeps it aligned with your strategy.

4️. It Maintains Target Allocation

Rebalancing ensures that your portfolio continues to reflect:

- Your risk tolerance

- Your time horizon

- Your original investment thesis

If you decided that 60% stocks and 40% bonds was appropriate for you, then letting it drift to 80% stocks changes the entire strategy. Rebalancing is about staying loyal to your plan. It enforces discipline automatically — without relying on emotions.

Final Thoughts on Portfolio Rebalancing

Rebalancing is not about chasing higher returns.

It is about:

- Controlling risk

- Preventing concentration

- Maintaining alignment with long-term goals

- Avoiding emotional decision-making

In short: Rebalancing protects your strategy more than it enhances your returns.

Frequently Asked Questions About Portfolio Rebalancing

1. How often should I rebalance my portfolio?

Most investors rebalance once per year. Another common approach is to rebalance whenever an asset allocation drifts more than 5–10% from its target. The best frequency depends on your strategy, transaction costs, and risk tolerance.

2. Does portfolio rebalancing improve returns?

Rebalancing does not guarantee higher returns. Its primary purpose is risk control. In strong bull markets it may slightly reduce returns because you trim winning assets, but it helps prevent excessive risk and large drawdowns.

3. What happens if I never rebalance?

If you never rebalance, your portfolio may gradually become concentrated in the best-performing asset. This increases volatility and downside risk. Over time, your portfolio can look very different from your original investment plan.

4. Is portfolio rebalancing necessary for long-term investors?

Yes, especially for diversified portfolios. Long-term investors benefit from maintaining their target allocation to control risk. Even a simple annual review can help keep your portfolio aligned with your financial goals.